The digital transformation of financial services has reshaped customer expectations, driving a demand for faster, more efficient, and transparent transactions.

At the forefront of this shift are real-time payment (RTP) systems, which empower individuals and businesses to transfer money within seconds, 24/7. It’s a revolution in how payments are made, unlocking revenue opportunities and forcing a new standard for payments companies under intense pressure to compete.

For businesses, RTP systems mean reduced settlement delays, improved cash flow management, and the ability to offer customers a seamless payment experience. By meeting the modern expectation of instant financial interactions, companies can enhance loyalty and trust. However, for payment providers, that expectation comes with an unforgiving demand for speed, precision, and control.

The instantaneous nature of RTP leaves little room for error and demands a robust, secure infrastructure. It opens the door to increased risks as fraudsters exploit rapid transaction speeds to bypass traditional fraud detection measures, leaving financial institutions and their customers vulnerable. Legacy tools can’t keep up, and without modern safeguards, fraud losses can escalate before anyone even knows a breach occurred. RTP providers could face significant losses and reputational damage due to sophisticated and evolving fraud tactics.

As RTP systems continue to gain traction globally, understanding their mechanisms, benefits, and risks is essential. By implementing advanced fraud prevention strategies that combine AI, behavioral analytics, and real-time monitoring, payments companies can strike a balance between innovation and security and avoid becoming the next cautionary tale in the race to modernization.

Understanding Real-Time Payments and the New Landscape

What is a Real-Time Payment?

A real-time payment (RTP) is the instantaneous transfer of funds from one account to another, supported by a highly efficient payment infrastructure that operates without interruptions. Unlike traditional payment methods, which may take hours or even days to process, RTP systems settle transactions in real time, ensuring that funds are immediately accessible to the recipient. This eliminates delays and offers a transformative solution for businesses, individuals, and governments. For payment providers, it’s not just a feature. It’s a foundational shift in customer expectations.

Key Features at a Glance

- Speed: Payments are processed within seconds, regardless of the time or day, including weekends and holidays. This is a game-changer for refund automation, merchant settlements, gig worker payouts, and time-critical transactions.

- Transparency: RTP systems offer complete visibility into the transaction lifecycle, providing the sender and recipient with instant updates. This transparency reduces guesswork and builds trust between parties.

- Certainty: Funds are available immediately after the transaction is completed. Both parties receive simultaneous confirmation, eliminating the uncertainty of pending payments in traditional systems.

Why Real-Time Payments Matter

RTP is more than just a faster way to transfer money—it is reshaping the global financial landscape. For businesses, RTP systems improve cash flow, streamline operations, and enable faster supplier payments. For individuals, they bring convenience and peace of mind, whether paying for emergencies, splitting a bill, or receiving a paycheck. In regions with limited access to traditional banking, RTP systems have become lifelines for financial inclusion, fostering economic growth and empowerment.

As the demand for speed, transparency, and certainty in payments continues to rise, RTP is no longer a luxury. It is becoming the standard for modern financial ecosystems, and for payment companies, keeping pace means rethinking risk, compliance, and operational agility.

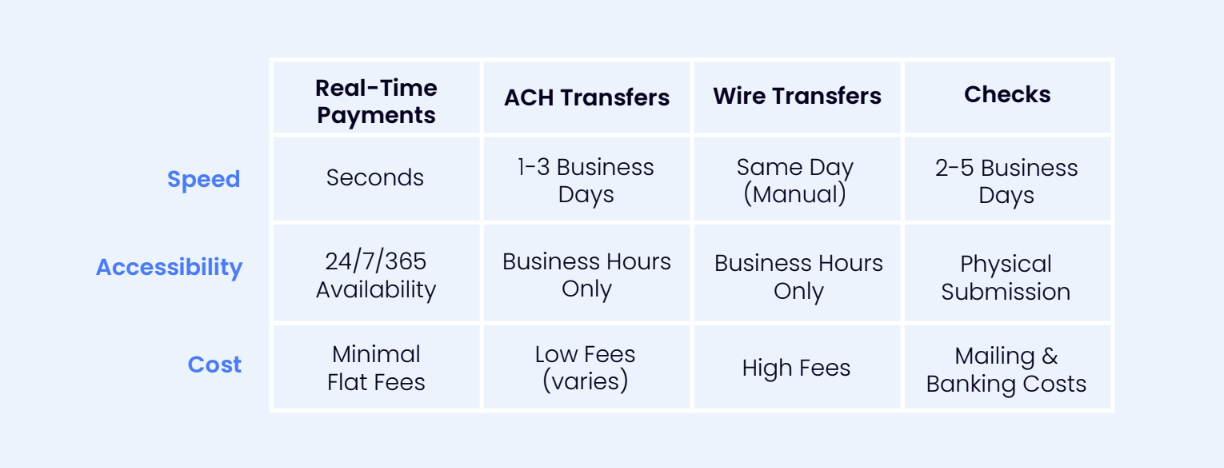

Comparing Real-Time Payments to Legacy Systems

The Cost of Relying on Legacy Systems

In today’s landscape, legacy systems don’t just slow you down - they put your business at a disadvantage. For example, an enterprise working with international suppliers using wire transfers, often faces delays of a day or more before payment clears, holding up shipping schedules and impacting supply chains. RTP eliminates this lag. Suppliers can receive payments instantly, at any time of day, allowing shipments to move faster and businesses to keep operations running smoothly.

RTP shines in speed and accessibility. Unlike ACH transfers that take days to process or wire transfers that require manual intervention, RTP offers efficiency at a fraction of the cost of traditional methods. Checks, while familiar, pale in comparison due to slow processing and higher associated overheads like mailing and handling.

Take, for example, The Clearing House's RTP Network in the United States. This innovative platform allows banks to process instant, direct account-to-account transfers, improving efficiency for both businesses and consumers. Similarly, Brazil’s Pix, launched by the Central Bank of Brazil, has revolutionized payments by enabling real-time transfers, even for the unbanked population. Pix’s accessibility has made it a vital tool for expanding financial inclusion, while demonstrating the scale and impact RTP systems can have when adoption is widespread.

Advantages of Real-Time Payments for Payment Firms

The benefits of RTP go far beyond convenience. They transform payment companies' operations, delivering measurable ROI, and reshaping customer expectations in the digital era. For firms managing high transaction volumes and complex compliance obligations, RTP can become the engine of growth.

Core Benefits

- Customer Experience: RTP enables instant refunds, drastically reducing churn rates. According to ACI Worldwide, 42% of customers are more likely to stay loyal to a brand if they receive refunds immediately. Immediate rewards also drive a stronger emotional connection, boosting long-term brand loyalty. For payments firms managing multiple merchants, this can be the difference between customer retention and churn.

- Cost Efficiency: RTP offers significantly lower transaction fees compared to traditional card networks, which can charge up to 3% per transaction. By leveraging RTP, businesses can save thousands annually, improving operating margins. NACHA reported that businesses using RTP saw a 25-30% reduction in overall payment processing costs. At scale, this represents millions in savings.

- Competitive Edge: Payment companies that integrate RTP attract more clients by offering faster, more efficient services. In fact, McKinsey found that 60% of businesses are actively seeking partners that provide real-time transaction capabilities, giving forward-looking payment providers decisive market advantages. Firms that lag in real-time capabilities risk falling behind as buyer expectations shift permanently.

How Industries Are Leveraging RTP:

- Gig Economy: Platforms like Uber have transformed the driver experience by enabling instant earnings disbursements after trips. This immediacy reduces financial strain for workers and fosters long-term loyalty, as drivers increasingly seek platforms that value their time and effort.

- Consumer Lending: Borrowers can access loan funds in seconds instead of days, alleviating financial stress during critical moments. For lenders, this speed increases competitiveness in a highly crowded market by offering unparalleled convenience.

- E-commerce: RTP is redefining online shopping through “Pay by Bank” at checkout, minimizing the need for credit cards and reducing merchant processing fees while giving customers a more straightforward, cost-effective payment option.

- B2B Reconciliations: Real-time visibility into receivables and payables empowers businesses to optimize cash flow. Corporations can reconcile accounts instantly, improving financial decision-making and productivity while reducing errors in payment tracking.

- International Commerce: Small exporters and businesses now avoid the high costs and delays of traditional cross-border payments. This democratization of international trade levels the playing field and enables smaller players to compete globally.

RTP’s Impact on Consumer Behavior:

Research by Deloitte found that RTP increases customer satisfaction by 73%, reducing waiting times and improving the purchasing experience. Additionally, a report by McKinsey highlights that 60% of consumers are more likely to choose retailers that offer RTP options. This shift in behavior underscores a deeper truth: convenience is now non-negotiable. Customers gravitate toward companies that prioritize convenience and responsiveness, and payments firms that enable this experience will define the next wave of industry leaders.

Inside the Ecosystem: The Platforms Powering Real-Time Payments

Key Players in RTP Systems

RTP systems have transformed the global financial landscape, with numerous players driving innovation to meet the needs of their respective regions. Here’s a deeper dive into some of the most influential players and their contributions to the industry:

- The Clearing House (U.S.):

As the operator behind the RTP Network, The Clearing House has been a pioneer in modernizing the U.S. payment ecosystem. Launched in 2017, the RTP Network provides real-time clearing and settlement for financial institutions of all sizes. It aims to enhance efficiency and transparency, offering features like immediate fund availability, payment tracking, and data-rich messaging.

- FedNow (U.S.):

Launched in 2023 by the Federal Reserve, FedNow is designed to broaden access to real-time payment infrastructure, especially for smaller financial institutions. It provides instant settlement capabilities, helping businesses improve cash flow and enabling consumers to access funds immediately. FedNow complements the RTP Network, giving financial institutions more options to adopt RTP.

- SWIFT and Cross-Border Innovations:

The SWIFT network continues to play a prominent role in facilitating international payments. Recent innovations, including SWIFT gpi (Global Payments Innovation), have improved cross-border payments' speed, transparency, and traceability. These advancements are driving efficiency for banks and businesses involved in global trade.

- Brazil’s Pix:

Introduced by the Central Bank of Brazil in 2020, Pix has become a revolutionary force in promoting financial inclusion. Designed for instant payments 24/7, it enables seamless peer-to-peer transfers, bill payments, and even payments to government entities. By eliminating fees for individuals and offering low-cost solutions for businesses, Pix has been instrumental in reducing reliance on cash and expanding access to digital financial services in underserved areas.

- India’s Unified Payments Interface (UPI):

UPI is perhaps one of the most successful RTP systems globally, processing over 10 billion transactions monthly as of 2023. Developed by the National Payments Corporation of India (NPCI), UPI enables interoperable payments across banks and apps. Its success lies in its simplicity, allowing users to transfer money using just a phone number or virtual payment address. UPI has also integrated advanced features like recurring payments, international transactions, and QR code compatibility, driving its widespread adoption.

- Europe’s SEPA Instant Credit Transfer (SCT Inst):

The European Payments Council (EPC) launched SCT Inst to enable instant euro transfers across participating countries. With a maximum processing time of 10 seconds, it supports cross-border payments within the Single Euro Payments Area (SEPA). This initiative has laid the foundation for more efficient regional trade and economic integration.

- Singapore’s FAST (Fast and Secure Transfers):

FAST is a real-time payment platform that enables instant bank-to-bank transfers in Singapore. Managed by the Association of Banks in Singapore (ABS), it supports various use cases, including peer-to-peer transactions, merchant payments, and business disbursements. Its integration with PayNow, a customer-friendly overlay service, has boosted adoption.

- Australia’s New Payments Platform (NPP):

Launched in 2018, NPP is Australia’s real-time payment infrastructure designed for speed, convenience, and data-rich transactions. With features like PayID, which links bank accounts to easy-to-remember identifiers such as phone numbers, NPP offers a user-friendly payment experience. It powers the country’s "Osko" service, enabling consumers and businesses to make and receive payments instantly.

- China’s Payment Giants (WeChat Pay and Alipay):

While not traditional RTP systems, WeChat Pay and Alipay dominate China’s digital payments ecosystem, facilitating real-time transfers between users and merchants. These platforms integrate with various services, from e-commerce to transportation, and have set a high standard for speed and convenience in mobile payments.

- UK’s Faster Payments Service (FPS):

Introduced in 2008, FPS was one of the earliest real-time payment systems. It allows instant transfers between UK banks, and its underlying infrastructure has been continuously updated to support growing demand. FPS has been a critical enabler of innovation in the UK’s fintech ecosystem.

- South Africa’s Real-Time Clearing (RTC):

Operated by BankServAfrica, RTC facilitates instant interbank transfers, helping to support the country’s growing digital economy. It has been a key driver in reducing reliance on cash and improving financial inclusion in South Africa.

- Mexico’s SPEI (Interbank Electronic Payment System):

Launched by the Bank of Mexico, SPEI allows real-time interbank transfers and has been instrumental in driving financial inclusion. It supports a wide range of use cases, from peer-to-peer payments to payroll and supplier payments for businesses.

- Canada’s Real-Time Rail (RTR):

RTR is Canada’s upcoming real-time payment system, developed by Payments Canada. Expected to launch soon, it focuses on speed, data-rich payments, and interoperability and aims to modernize Canada’s payment infrastructure and support economic growth.

...Continue reading this ebook to learn about:

- Emerging technologies shaping RTP's future.

- Fraud and compliance risks with Real-Time Payments.

- 6 essential solutions for mitigating fraud and risk.

- Fraudnet’s end-to-end platform for real-Time fraud, risk, and compliance.

- and more.

%20(640%20x%201229%20px).png)

You might be interested in…

Get Started Today

Experience how FraudNet can help you reduce fraud, stay compliant, and protect your business and bottom line